Features

Columns

Education

Money Matters: What comes next?

What keeps an aggregates business owner up at night.

July 30, 2015 By Jim Sanderson

“Hop in,” John said.

We drove by the scale house to see his baby: a 475,000 ton/year operation that has been supplying aggregate to projects across the Greater Toronto Area (GTA) for more than three decades.

“Thanks for coming up,” he said. “We’re all busy.” John mentions his wife Terri, who runs the administrative work. “We aren’t getting any younger and the business has been growing like wildfire with the expansion of the GTA.”

We came to a stop in front of the main entrance to his operation.

“Before you tell me how you built this great business I would really like to know what’s keeping you up at night,” I said. I expected him to give me the standard answer that everything was fantastic. Instead, he put his truck in park and began to describe what was often robbing him of sleep. He clearly wanted to talk.

“What worries me most is that I have a responsibility to our workers and their families. I am getting tired. I don’t know who is going to take over now that our son, Billy, has moved out West. No buyers come to mind, but I want to get a good price if I do sell. It’s not that we want to close the business tomorrow, but I do want to slow down. It’s hard to relax when you don’t know what’s going to happen next – in your life and business.”

That was big, from the heart information. I pulled out my digital recorder and requested permission to capture everything he was going to tell me so I didn’t miss anything.

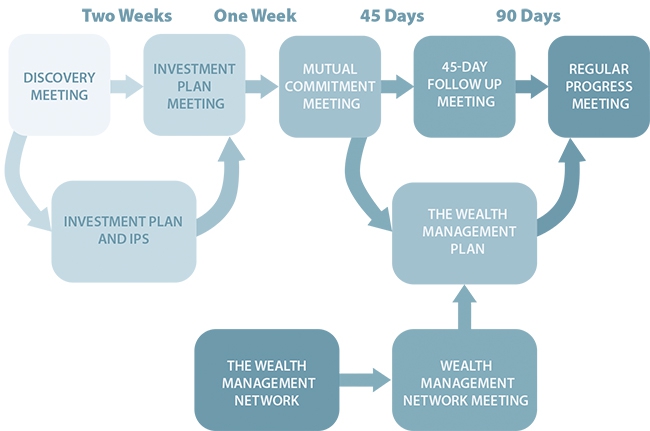

“Thanks for calling me, John,” I said. “Let’s go through this one step at a time… tell me how all of this got started.” And for most of my business owner clients, that’s usually how the business planning process begins.

John needs help, but is too busy to even begin to look for it. He told me both his and the company’s story. He is really a farmer first, loves horses and built a business by working hard and helping people and his community. After almost two hours, and a three-hour drive back to the office, I started to highlight some steps to help him ensure that his years of hard work pay off when he decides to sell or retire – on his terms. These include:

- Setting up a holding company to minimize tax issues,

- Beginning to build an investment portfolio to generate cash flow outside the business,

- Generating cash from inside the business in a consistent and tax-effective ways,

- Creating a succession plan – even if there are no successors or buyers at the moment,

- Minimizing risk to him, his family and his business by purchasing critical illness insurance and making sure he was well insured.

Get a handle on the tax load

“How about first getting a handle on my tax load?” John asked. “I can’t seem to get ahead.”

I suggested that a holding company could be set up to protect him from unnecessary tax issues.

“It sounds complicated and seems to involve more work,” John said.

“It’s true,” I said. “It’s not easy to set up a holding company [holdco]. Creating a holdco can be expensive, as you must provide annual financial statements and corporate tax returns. If your shares are not of significant value, a holding company may create more headaches than peace of mind.”

I suggested there were other issues to consider. For example, tax benefits may not exist, or worse, tax problems may arise as a result of setting up a holdco.

It is important to remember that any losses realized in a corporation are only available to offset other income earned by the corporation.

And, the $750,000 capital gains deduction does not apply to holding companies.

A holding company may also trigger an additional level of tax in addition to any personal income tax on distributions from the holding company.

I said he would need to consider tax-efficient ways to distribute assets from his holding company to shareholders to avoid a negative tax event, and that can take time and money.

“Now, tell me the good news about holdcos,” John said.

“For starters, your holdco could help you lower your risk by protecting your business from creditors while letting you enjoy the benefits of the operating company’s goodwill,” I said.

When shareholders are faced with a high marginal tax rate, they may defer a portion of tax on dividends from taxable Canadian companies until dividends are paid by the holding company to the shareholders.

A holding company may also help ease the transfer of wealth to family and other beneficiaries. For example, John might be able to transfer shares in his operating company to his children through his holding company using an estate freeze. (Estate freezes essentially put a ceiling on a person’s tax liability upon his or her death and transfers any future cash gains within the operating company to his or her beneficiaries.)

Control your investments

John acknowledged that his investments were “all over the place” and that different companies were charging him high management fees. “Some of my money is invested in mutual funds with different names, but I really don’t know where the money is. And I have no idea how my investments are doing.”

His business’ retained earnings are also in disarray. They aren’t diversified and were limiting him to short-term investments, which were earning him very little after tax.

He liked the idea of a well-diversified investment portfolio where costs are low and closely monitored by a financial advisor.

Introduce a succession plan

“What about the future of my business?” he asked. “What will I have to show for all the years I’ve put in?”

He could begin planning by identifying his priorities and a buyer or successor, and developing a succession plan. “You will need to keep your personal retirement and estate goals in sync with your succession plan to stay on track,” I said.

“By the way, if you take on shareholders, you would be amazed how many business owners don’t have a signed shareholders’ agreement. A signed agreement takes the guesswork out of a situation that you wish will never happen. It’s like a roadmap.”

Insurance is a valuable asset

“I mentioned my health concerns,” John said. “What about insurance?”

While it seems fairly practical, it’s not free. Policy costs will likely mirror similar coverage on the personal side but who, how and when it would pay out is a little more complicated due to tax issues.

The deductibility of insurance premiums and taxability of benefits is highly dependent on the type of coverage and the type of payout and beneficiary.

“Where possible, insure and pay for your personal life policies personally and insure and pay for your key person insurance corporately, and keep it as simple as your business structure allows.”

A critical illness policy provides John with a lump sum benefit, if he is diagnosed with a critical illness.

Source: http://www.canadabusiness.ca/eng/page/2684/

Whether he plans to gift the ownership of his business when he dies or plans to institute an estate freeze strategy, the proceeds of a life insurance policy can be used to help cover the taxes payable resulting from the years of growth of his business. A life insurance policy can also ensure that each heir receives their fair share of John’s estate and possibly increase the amount of money he leaves behind.

After we finished our coffee and our visit for that day came to an end, John thanked me again for meeting with him and wished me a safe drive home. He seemed more relaxed than when I arrived. We agreed to meet again with his wife a few weeks later to make sure I understood exactly what was important to both of them. While he realized that everything couldn’t be done overnight, he said he finally felt focused and ready to move forward with some careful planning to make the most of his years of hard work.

Jim Sanderson is a wealth advisor team with 28 years in the investment services industry. The Jim Sanderson Group at ScotiaMcLeod specializes in creating and distributing wealth for successful individuals and corporations in the aggregate and road building industries across Canada. He helps his clients supported by a team of experts in insurance, merchant banking, trust and estates. Jim can be reached at jim.sanderson@scotiamcleod.com and his website is located at www.jimsandersongroup.com.

Print this page